Farming is a Volatile Low-Margin Business

There are hundreds of thousands of farmers in the United States, many of them producing the same product as their neighbor. They have ample information about global markets for their product and can start or stop farming whenever they like.

These characteristics describe a perfectly competitive market. As every economics student learns, no-one consistently makes large profits in a perfectly competitive market. They make enough to fairly compensate them for their time and investment and that is it.

So, is it true that American farmers make low profits?

One place to look for the answer is the Farm Income and Wealth Statistics produced by the Economic Research Service of the USDA.

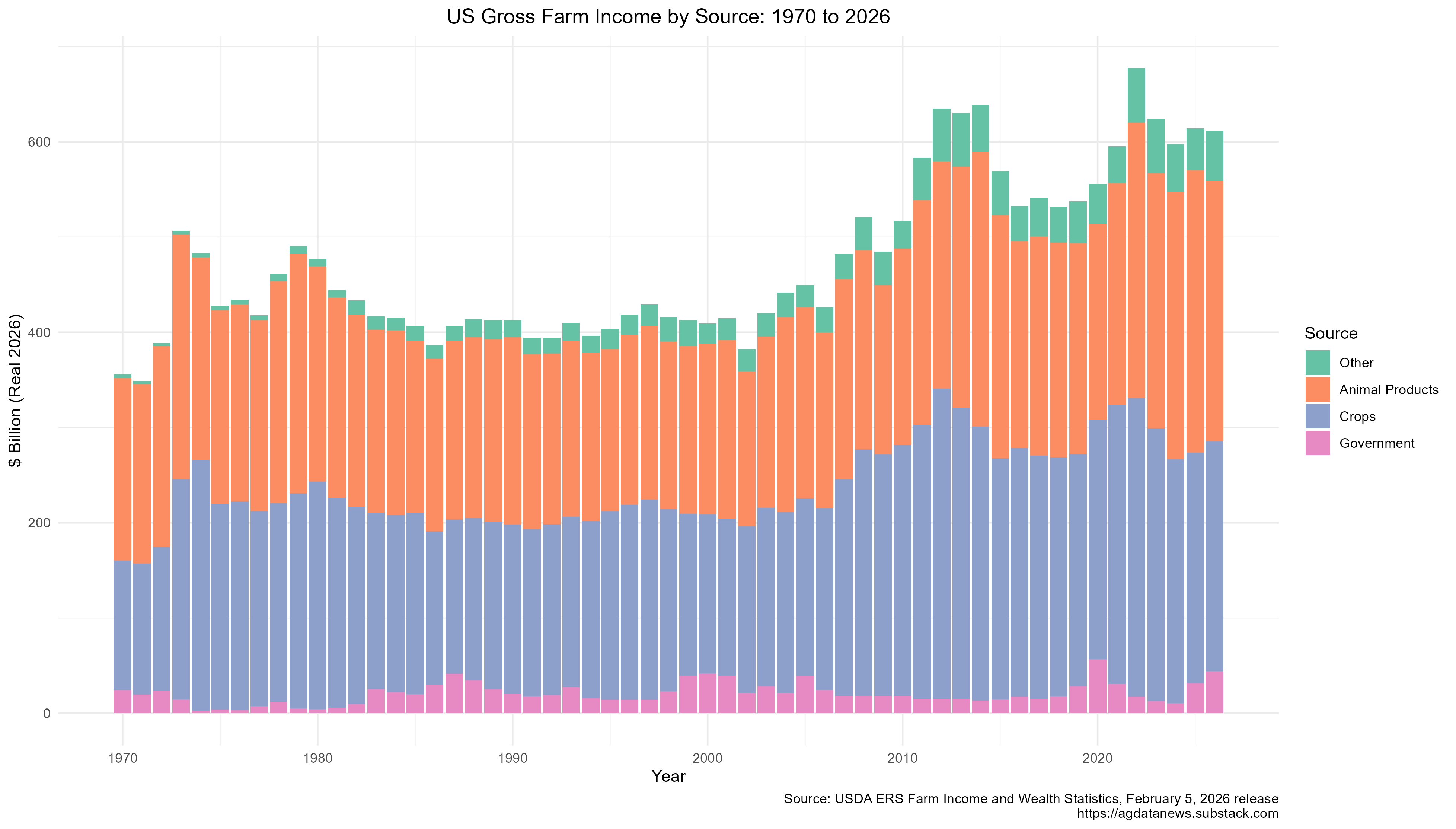

Let’s start with gross farm income. American farmers received gross revenue of about $600 billion in each of the last six years, which is 2% of GDP. Crops and animal products each account for 45% of this revenue, and government payments accounted for 4%.

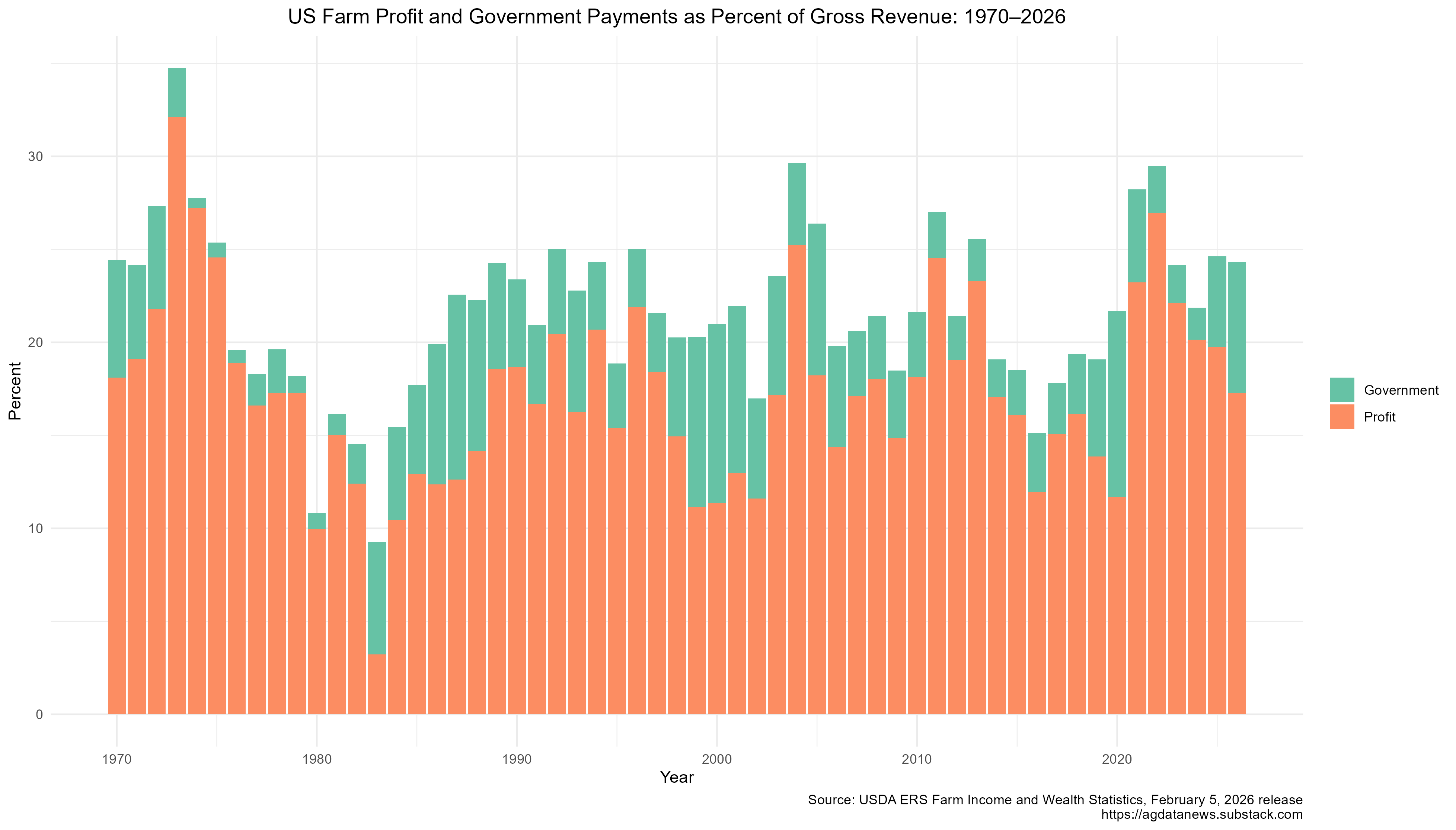

Some gross income goes to pay for inputs like fertilizer and seed, and some of it goes to profit. On average, net profits are 21% of gross farm income. After subtracting government payments, net profit from market sales is 17% of gross revenue. These are high percentages. The average net profit margin in the US economy is 10%. Grocery stores, which are the prototypical low-margin industry, have a net profit margin of 1%.

If net profit margin is 17%, why do I say farming is a low margin business?

Farmers make money in two ways. They own land that goes up in value and they sell agricultural products. The second part is the business of farming and that is where the low margins are.

Land owned by the farmer is not free. If they didn’t farm on it, they could rent it to someone else. They are giving up that income when they choose to farm on it. So, we should add foregone land rent to production costs, which reduces the profit margin.

The same argument applies to the farmer’s time (and the time of family members and others who give unpaid labor to the farm). If they weren’t working on the farm, they could work elsewhere for a wage.

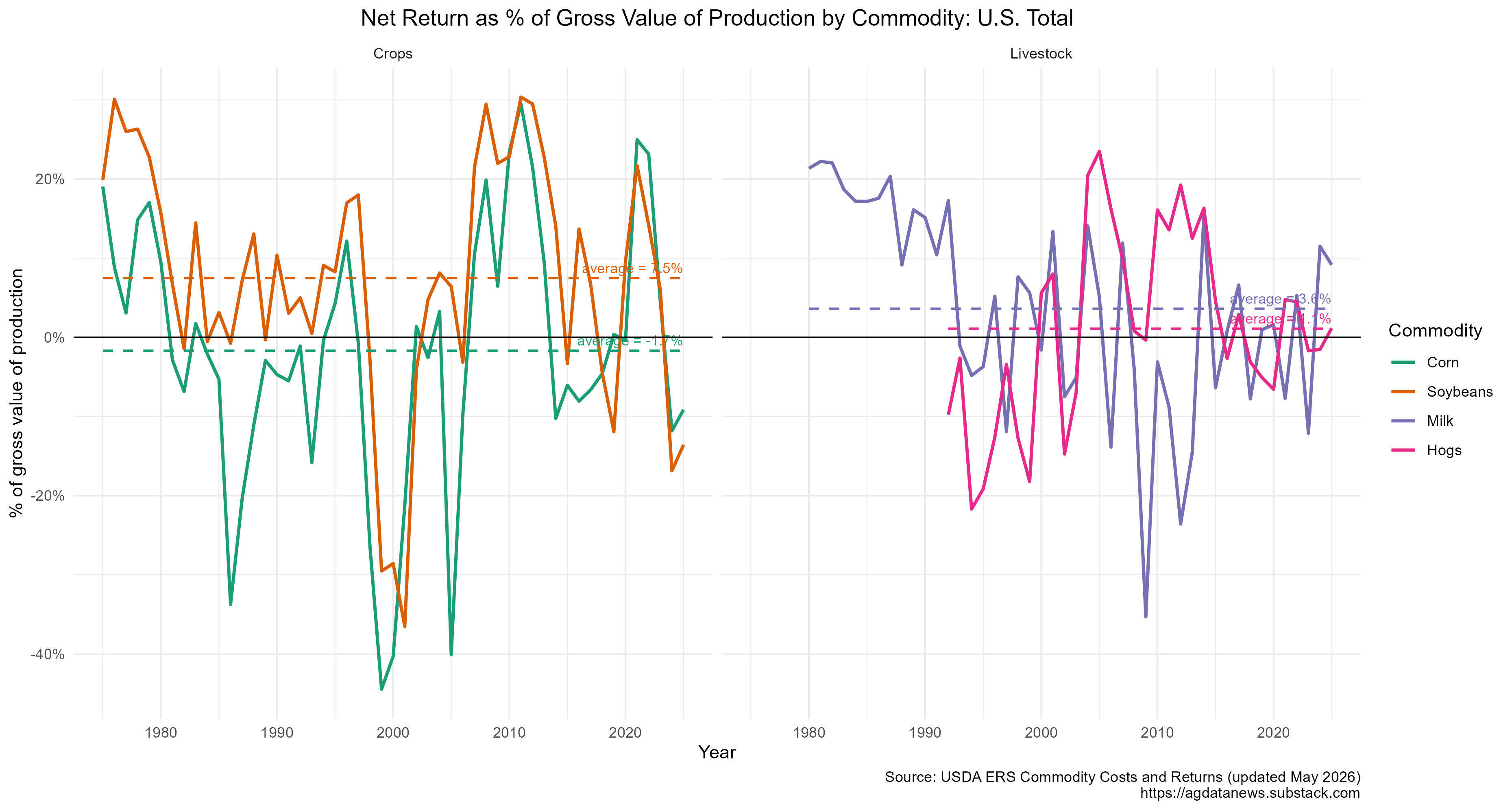

USDA publishes estimated costs and returns for producing various commodities. These data count opportunity costs of owned land and unpaid labor as costs to the farm business. They exclude government payments.

Over the last 50 years average net profits for soybeans were 7% of the value of production. Average returns for corn were -1.2%, and average returns for milk and hogs were both less than 5%. The business of farming is indeed a low-margin business.

In contrast to overall farm profit, commodity-specific net returns are very volatile. Corn grower losses were 40% of revenue in 2005 and their profits were 20% of revenue in 2011, as shown above. Overall farm profits are never negative and were only below 10% of revenue in one year (1983).

So, individual farmers face significant ups and downs from year to year, but fortunes average out across farmers. Corn and soybean growers lost money in 2024 and 2025, but cattle farmers made high profits in those years.

So, are farmers poor?

No. Most commercial farmers own a valuable asset (farmland) that tends to increase in value. USDA ERS reports that “households operating commercial farms (those with gross cash farm income of at least $350,000) had $3.9 million in total wealth at the median, substantially more than the households of residence or intermediate farms.”

In 2024, ERS reports that more than 97% of farm households had more wealth than the median household. Also in that year, 40% of farm households had below-median income. Farming is a low-margin volatile business.

Some of you may be thinking of farmers you know who have made large profits. Look deeper, and you will probably see conditions that diverge from the perfect competition model. For example, a farmer may be first to use a productive new technology. They can reap profits from being better than everyone else, but soon others catch up and we are back to competition and low profits.

For another example, many California farmers made large profits on almonds and pistachios in the last 20 years. Supply was constrained by the fact that it takes several years for nut trees to reach bearing age after they are planted. But, eventually farmers produce more of highly profitable crops, creating extra supply that reduces the price and eliminates the profits, as has happened in almonds.

In summary

Low profits are intrinsic to commodity farming, yet our politics are beset by the sentiment that farmers don’t make enough money. The problem is that, whenever farm profits appear, they disappear just as quickly into the value of farmland or are captured by seed companies, fertilizer companies, or other suppliers.

Trying to persistently increase farm profits is a fool’s errand that policy makers have been chasing for decades.

I made the graphs using this R code.

Interesting article. A discussion about ROI and cash flow challenges on farms would also be interesting.